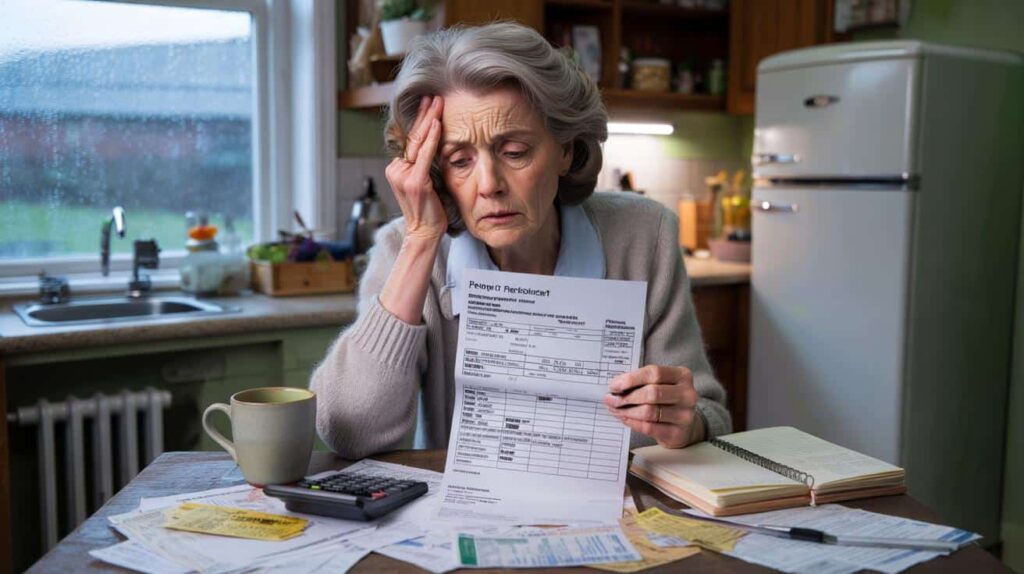

The letter arrived on a rainy Tuesday morning when the sky hung low & heavy over the street. Margaret stood in her hallway with the envelope half torn and her glasses slipping down her nose. She read the same line over and over: “Your state pension will be reduced by £140 per month from February.” The kettle clicked off behind her but she didn’t move. She was already doing the quick maths in her head. One week’s food shop. Two direct debits. The gas bill. Gone.

She put the letter on the kitchen table next to a pile of supermarket coupons and circled prices in the brochure out of habit. A small luxury here, a brand-name product there, suddenly felt like a risk. Pension cuts aren’t just numbers. They creep into your fridge, your thermostat, your sleep.

And this time, the cut is official. Approved. Coming in February.

A £140 shock: what this state pension cut really means

Across the UK, retirees are opening almost identical letters, each carrying the same short, blunt message. A state pension cut has now been approved, slicing an average of **£140 a month** from payments starting in February. On paper, it looks like a line item in a budget. In real life, it feels like losing a small but vital piece of freedom.

For many people that £140 makes the difference between feeling reasonably secure and feeling constantly worried. Bills are already going up. Food prices remain high. Council tax notices will arrive soon. The cut happens right in the middle of all that financial pressure. Without any fuss or attention it forces thousands of older people to change how they live each day.

Look at the numbers and the story sharpens. An average full state pension is a little over £800 a month for many retirees. Take away £140 and you’re suddenly closer to £660. That’s not a minor trim. That’s more than 15% gone in one stroke, at a time when private savings for a lot of people are already thin or completely exhausted. For someone renting, with no other income, the budget simply doesn’t stretch. Something has to give. Heat. Food. Social life. Dignity.

We have all experienced that moment when a bank balance falls lower than expected and causes a brief moment of worry. For pensioners affected by this cut that feeling will not be temporary. It risks becoming part of their everyday life. The reduction in pension payments means many elderly people will face ongoing financial stress rather than just occasional concern about money. What most people experience as a passing worry could become a constant source of anxiety for those living on fixed retirement incomes. This change affects how pensioners manage their daily expenses and plan for basic needs. The financial pressure does not come and go like it might for working people who have other income options. Instead it becomes a persistent challenge that shapes their daily decisions about spending on essentials like heating food and medicine.

From letters to lives: how a £140 cut hits real people

Picture a small flat on the edge of Leeds. James, 68, ex-bus driver, boils his tea while tracing his finger down a notebook of outgoing payments. Rent, electricity, mobile, prescriptions. After the new pension figure, he’s left with roughly £45 a week for food, toiletries, bus fares, and anything unexpected. He crosses out the Friday fish and chips he usually treats himself to. Then he crosses out the monthly visit to see his sister two towns over.

It’s easy to throw statistics around. It’s harder to admit that for thousands, the “non-essentials” now under threat are actually the small things that stop life from feeling purely mechanical. A weekly café visit. A warm bathroom in the morning. The chance to say yes to a grandchild’s birthday outing instead of inventing an excuse. *You don’t see that on a government spreadsheet.*

Charities are already reporting more calls about fuel debt & food banks from older people who had never asked for help until recently. One national ageing charity says demand for its helpline has jumped significantly since news of the cut leaked out. These are not people looking for handouts but asking how to survive a permanent drop in income when prices feel permanently high. Nobody really does a full professional household budget every single day. Most of us juggle and guess. When a cut like this hits the guesswork suddenly turns risky.

# Why Gardeners Hang Cork Stoppers on Lemon Branches

Many gardeners who grow lemon trees have discovered an unusual but effective trick. They hang cork stoppers on the branches of their lemon plants. At first glance this practice might seem strange or even pointless. However there is solid reasoning behind this method that has been passed down through generations of experienced growers.

## The Main Purpose Behind Cork Stoppers

The primary reason gardeners use cork stoppers on lemon branches relates to pest control. Lemon trees attract various insects that can damage the fruit and leaves. Cork has natural properties that certain pests find unappealing. When hung on branches the cork acts as a gentle deterrent without using harsh chemicals. Cork also absorbs moisture from the air. In humid conditions this can help prevent fungal growth on the branches. The material creates a small barrier that discourages harmful organisms from settling on the tree. This simple addition provides protection while remaining completely natural and safe for the plant.

## Additional Benefits of Using Cork

Beyond pest control cork stoppers serve other useful functions. They can mark specific branches that need attention or special care. Gardeners often use them to identify branches they plan to prune or ones that produced particularly good fruit. This visual marker system helps keep track of the tree’s development over time. The lightweight nature of cork means it does not damage delicate branches. Unlike heavier objects that might bend or break young growth cork stoppers stay in place without causing harm. They weather outdoor conditions well & last for multiple growing seasons.

## How to Apply This Method

Implementing this technique requires minimal effort. Gardeners simply pierce the cork stopper with wire or string and attach it loosely to selected branches. The cork should hang freely rather than being tied tightly against the branch. This allows air circulation while keeping the cork in position. Most gardeners place cork stoppers on lower branches where pests typically enter the tree first. Spacing them evenly throughout the canopy provides broader protection. Replacing the corks annually ensures they maintain their effectiveness as they gradually break down from exposure to weather. This traditional gardening practice demonstrates how simple natural materials can solve common problems. Cork stoppers offer an affordable & environmentally friendly way to protect lemon trees while avoiding synthetic pesticides.

➡️ Goodbye balayage: “melting,” the new coloring technique that makes gray hair almost unnoticeable

➡️ Goodbye to grey hair : the trick to add to your shampoo to revive and darken your mane

➡️ The RSPCA urges anyone with robins in their garden to put out this simple kitchen staple to help birds cope right now

➡️ Psychology says quiet people who observe more than they speak read your feelings and secrets while talkers stay blind

➡️ Neither swimming nor Pilates: new research crowns a brutal workout as the best for knee pain and sufferers feel betrayed

# Aluminium Foil in the Freezer: A Simple Trick That More People Are Using

Many households are discovering a practical use for aluminium foil that goes beyond wrapping leftovers. Placing aluminium foil in your freezer might seem unusual at first but this method offers several benefits that make it worth trying. The main advantage of using aluminium foil in the freezer relates to temperature regulation. When you place sheets of aluminium foil on the freezer shelves or walls the material helps distribute cold air more evenly throughout the space. This happens because aluminium is an excellent conductor of temperature. The foil absorbs the cold & spreads it around which means your frozen foods stay at a more consistent temperature. Another benefit involves energy efficiency. When your freezer maintains a more stable temperature the compressor doesn’t have to work as hard to keep things cold. This can lead to lower electricity bills over time. The foil essentially acts as a thermal mass that helps retain the cold when you open the freezer door. Some people also use aluminium foil to prevent frost buildup in certain areas of their freezer. By lining problem spots where ice tends to accumulate you can make defrosting easier & less frequent. The smooth surface of the foil makes it harder for moisture to stick and form thick layers of ice. This trick works best when you use heavy-duty aluminium foil rather than the thin variety. Simply cut pieces to fit your freezer shelves or the areas where you want better temperature control. You can secure the foil with tape if needed though many people find it stays in place on its own. While this method won’t solve every freezer problem it offers a simple and inexpensive way to improve how your appliance functions. More households are adopting this approach as they learn about its practical advantages.

➡️ In two weeks, the Game of Thrones universe returns with an all-new series!

Behind the scenes, the logic from policymakers is all about “sustainability” and “balancing the books”. An ageing population, rising health and social care costs, pressure on public finances. On a macro level, the sums might add up. On a human level, the move sends a very different message: that the most reliable part of older people’s income can be moved down a notch, even as everything else moves up. That mismatch between official language and lived reality is where anger, and quiet fear, tend to grow.

What can pensioners actually do now?

When a cut is already approved, you can’t reverse it from the kitchen table, but you can change how exposed you are to it. The first concrete step is unglamorous: write everything down. One month, every pound. State pension, private pension, part-time work, benefits. Then list rent or mortgage, council tax, utilities, insurance, travel, food, debts. Seeing it all in black and white is uncomfortable, yet that’s where your real options start to appear.

From there, the next step is to check whether you’re claiming every entitlement linked to your situation. Many older people don’t realise that a lower pension payment can open (or widen) doors to extra support. That might include Pension Credit, Housing Benefit, Council Tax Support, or disability-related payments. Talking to a local Citizens Advice, Age UK, or a welfare rights adviser can turn into real money each month, not just theory. Some pensioners discover they’ve missed out on support for years.

The temptation right now is to panic and cut everything that looks “non-essential”. That instinct is understandable, but it can backfire. Slashing heating too hard in February can fuel health problems that cost more in every sense. Dropping all social activities can worsen anxiety and depression. A better way is a priority ladder. Top rung: staying warm enough, housed, safe, with food in the cupboard. Middle rung: stable routines like small outings, hobby groups, digital access. Bottom rung: subscriptions you barely use, impulse shopping, branded items you don’t really need.

And if your budget is already stripped to the bone, earning a little extra might feel out of reach, yet for some it’s still an option. A few hours a week in a charity shop, online selling, or local childcare can plug part of that £140 gap. Not everyone is healthy enough to work longer. For those who are, even a tiny, regular extra income can calm that month-end dread.

The emotional side is just as real as the numbers. Shame is a big silencer here. Plenty of people in their 60s, 70s and 80s were raised to “just cope” and not talk about money. They feel embarrassed to say, “My pension has been cut and I’m struggling.” That silence keeps people isolated. It also lets bad policy slide past without noise. If your outgoings no longer fit your pension, it’s not a personal failure. It’s a structural squeeze landing in your living room.

There’s also a subtle danger: cutting back so far that life loses colour. Humans are not designed to live purely on survival mode. A monthly craft group, a Sunday paper, streaming a favourite series, these are not moral luxuries; they’re lifelines. The trick is to protect a small, sustainable slice of joy rather than wiping it out altogether. When money feels tight, your world can shrink. Guard against that, as fiercely as you tweak direct debits and hunt discounts.

The people who are directly affected are beginning to speak up. At a community centre in Birmingham a retired nurse explained it in straightforward terms.

“I worked and paid in for 45 years,” she said, folding her arms. “You plan your life around that state pension. Then they say, ‘Sorry, we’re taking £140 back every month,’ like it’s pocket change. It’s not pocket change to me. It’s my food, it’s my bus pass, it’s whether I put the heating on in the morning.”

# Looking Ahead: Practical Steps to Take Now

For anyone trying to navigate the months ahead there are some practical levers worth checking regularly. First focus on your financial foundation. Review your emergency fund & make sure it covers at least three to six months of essential expenses. This buffer provides security when unexpected situations arise. Look at your monthly spending patterns & identify areas where you can reduce costs without significantly affecting your quality of life. Next examine your income sources. Consider whether you can diversify how you earn money. This might mean developing a side skill or exploring freelance opportunities in your field. Having multiple income streams creates stability even when one source becomes uncertain. Your professional development deserves attention too. Update your resume and keep your professional network active. Reach out to former colleagues and attend industry events when possible. These connections often lead to opportunities you might not find through traditional job searches. Take time to assess your debt situation. High-interest debt should be your priority for paydown. Consider refinancing options if interest rates work in your favor. Creating a clear debt reduction plan helps you make steady progress rather than feeling overwhelmed. Your health & insurance coverage need regular review as well. Make sure your policies still match your current needs. Schedule preventive care appointments & address any medical concerns before they become serious problems. Finally build flexibility into your plans. The ability to adapt quickly matters more than having a perfect long-term strategy. Keep your skills current & stay informed about changes in your industry. This preparation helps you respond effectively when circumstances shift.

- Check your full state pension record and forecast online for errors.

- Apply for Pension Credit if you’re anywhere near the threshold.

- Ask your council about local energy, hardship or discretionary funds.

- Speak to your bank about breathing space on overdrafts or small debts.

- Join local community groups offering warm spaces and low-cost meals.

What this cut really says about ageing, value, and security

Behind every £140 cut in February lies a more fundamental question about the kind of old age people should have after working and paying taxes for decades. The state pension was designed to be a foundation that people could depend on when their savings were gone and their working years had ended and their health had declined. When that foundation becomes unstable the entire system loses credibility. People in their 40s & 50s are also paying attention and asking themselves what kind of retirement awaits them.

This isn’t just a technical adjustment; it’s a signal. It says: even the most basic promise can be thinned out when the sums higher up the chain don’t quite work. Some will respond with anger. Some with resignation. Some with activism, petitions, and campaigns to reverse or soften the blow. It may push more retirees into political life than any speech or rally ever could.

For now, the practical reality is stark: February’s payment will be smaller. Budgets will be rewritten. Small plans will be cancelled. Yet there is also a quieter, collective response taking shape. Families are talking more openly about money. Communities are setting up warm hubs and shared meals. Online groups are swapping tips on energy use, benefits, and side incomes. The cut hurts, no question. What comes next, in households and in politics, is still unwritten.

How people respond to this moment will reveal much about the country’s relationship with aging. Some will quietly adapt while others will loudly protest or carefully plan around it. This reaction matters not just for this winter but for the years that follow. The way citizens handle this situation shows their deeper attitudes toward getting older. Whether they accept changes without complaint or push back against them tells an important story. Those who take time to strategize and prepare demonstrate yet another approach to dealing with age-related challenges. These different responses provide insight into how society views its older population. The choices people make now will shape policies and attitudes for a long time. Understanding these reactions helps predict how the nation will address aging issues in the future.

| Key point | Detail | Value for the reader |

|---|---|---|

| Size and timing of the cut | Approved reduction of around **£140 per month** from state pension payments starting in February | Helps readers anticipate the exact scale and timing of the impact on their own budget |

| Real-life budget impact | Typical full state pension dropping from just over £800 to around £660 for many, squeezing essentials | Transforms an abstract policy into concrete numbers that can be compared to personal costs |

| Practical coping steps | Detailed checklist: full budget review, benefit checks, local support, small income options, and emotional support | Gives readers immediate, actionable starting points rather than just bad news |

FAQ:

- Will every pensioner lose exactly £140 a month?Not necessarily. £140 is an average figure associated with the approved change. The exact reduction depends on your entitlement, previous contributions, and whether you receive additional pension or benefits that may partly offset the cut.

- Does the cut affect existing Pension Credit or Housing Benefit?The lower state pension amount can change how means-tested benefits are calculated. In some cases, you might qualify for Pension Credit or a higher rate than before, so it’s worth doing a full benefits check.

- Can this pension cut still be reversed?Formally it has been approved, so it will apply from February unless new legislation or a policy U-turn is passed. Campaigns, media pressure, and political lobbying can sometimes change the landscape, but you should plan as if the cut is going ahead.

- What if I already struggle with bills before the cut?Contact your local Citizens Advice or Age UK as soon as you can. They can look at debt options, hardship funds, energy grants and benefit entitlements. Early advice usually gives you more room to manoeuvre.

- Is there any point in checking my National Insurance record now?Yes. Errors or gaps in your record can sometimes be fixed, which could slightly raise your state pension. It won’t cancel the cut, but it might reduce its impact over the long term.